A Guide to Working Capital Loans

Quick Answer

Key Takeaways

- Working capital = current assets minus current liabilities. A positive result means you can cover short-term costs without borrowing.

- Common triggers for working capital loans: slow-paying clients, seasonal demand swings, sudden growth, and unexpected expenses.

- A credit line suits businesses with recurring or unpredictable cash needs. Meanwhile, invoice financing and PO financing are best for businesses with receivables.

- It's best to borrow only the actual amount you need to fill a specific gap, and repay as soon as regular cash flow resumes. Overborrowing increases your interest without adding actual business value.

- Online business lenders like First Circle are more accessible than traditional banks: no collateral, faster approval, and less paperwork.

- First Circle's non-collateral Business Credit Line provides up to ₱20 million in capital for as low as 0.99% monthly interest. Get approved in as fast as 1-2 business days.

Every business owner knows the feeling: sales are coming in, orders are piling up — and yet somehow, there's not enough cash to cover payroll this week. That gap between money going out and money coming in is a working capital problem, and it's one of the most common reasons otherwise profitable SMEs stall or miss growth opportunities. Managing it well is the difference between a business that scales versus one that's always playing catch-up.

Read on to learn what working capital, why managing it is the best thing you can do for your business, and when it's time to take out a working capital loan.

What Is Working Capital and Why Does It Matter for Your Business?

Working capital is the money available to fund your day-to-day operations — payroll, supplier payments, rent, and utilities. You calculate it by subtracting your current liabilities from your current assets:

Working capital = Current assets − Current liabilities

A positive working capital means your business can meet short-term obligations without borrowing. A negative figure is a warning sign: you may not be able to pay bills on time.

Most financial advisors recommend holding at least one to three months of operating expenses in reserve. The right amount will depend on how predictable your revenue is, and how long clients typically take to pay. Businesses with long payment cycles — such as B2B suppliers, contractors, or exporters — need larger buffers than retail or service businesses that collect payment on the spot.

When Should You Take Out a Working Capital Loan?

Maybe your business just wasn't able to collect on receivables in time to fund an upcoming big project. Or rent and utilities are due at the same time as your accounts payable. Either way, a working capital loan can help you deal with temporary cash flow gaps that threaten your ability to operate.

A working capital loan is NOT a long-term substitute for healthy cash flow. At the same time, taking out one isn't an indication that your business is in poor financial health. Cash flow gaps usually happen due to mismatched timing: money isn't coming into your business as fast as money going out.

Here are the situations that most clearly call for a working capital loan:

- Inconsistent cash flow. Clients pay late, but your payroll, utilities, rent, suppliers, and other immediate business expenses cannot wait.

- Seasonal sales fluctuations. Businesses with pronounced high and low seasons — such as retail, agriculture, construction, and events — often need financing during slow months to maintain operations until peak revenue returns.

- New business opportunities. New contracts, bulk orders, and expansion all require upfront spending before income arrives. A working capital loan can cover payroll, fulfillment, and marketing in the meantime.

- Unexpected expenses. Equipment failure, supply chain disruptions, and emergency costs happen without warning

Rule of thumb: To keep your interest rate and monthly repayment low, borrow only the amount you need to fill a specific gap. Repay as soon as your regular cash flow resumes.

For first-time borrowers, learn the basics of business loans here.

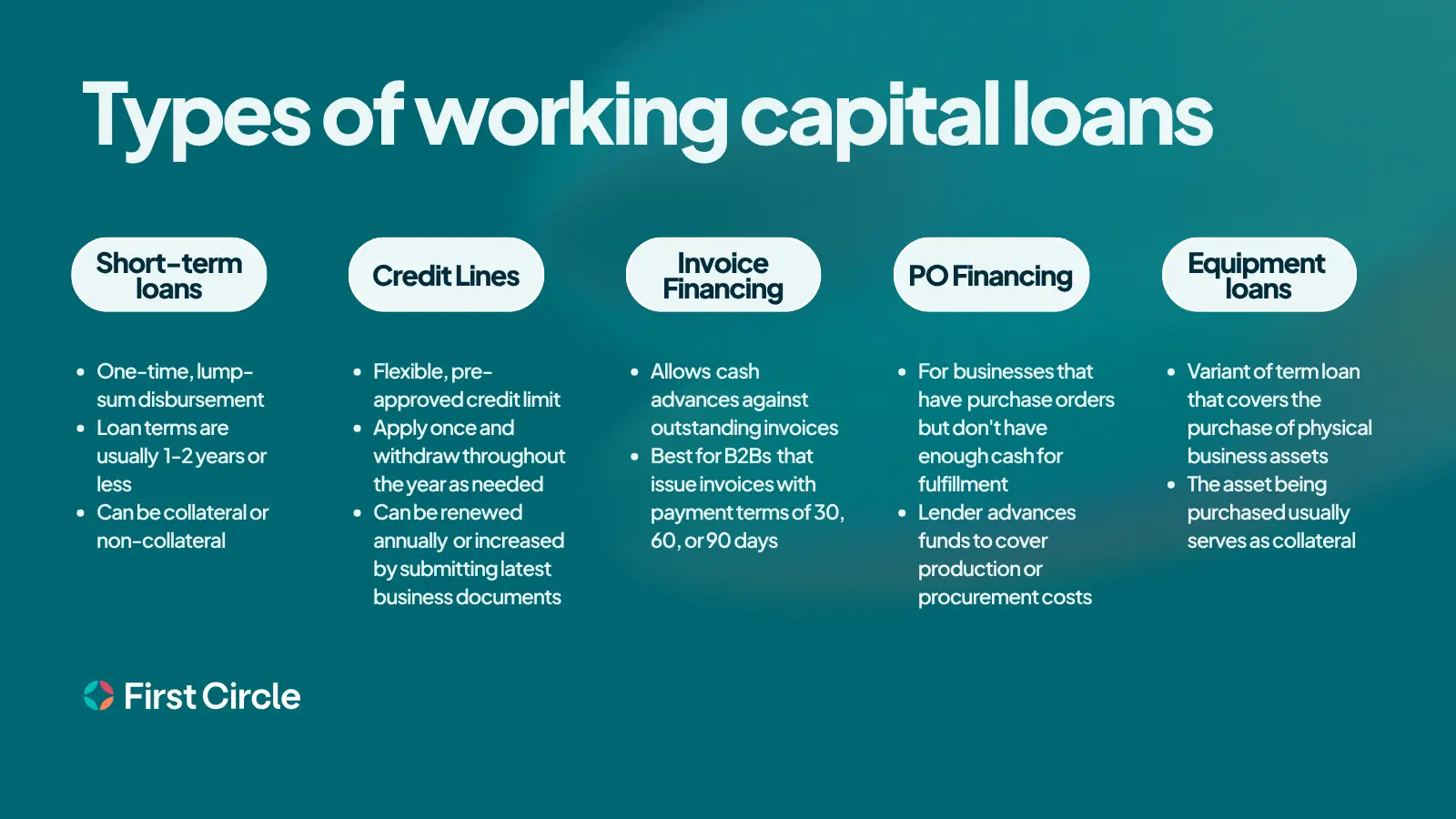

What Are the Types of Working Capital Loans in the Philippines?

Short-Term Loan

Short-term business loans are lump-sum disbursements repaid in fixed monthly installments — typically over 6-12 months. They are best suited to one-time, defined needs such as a specific equipment purchase, a seasonal inventory build-up, or bridge financing before a large client payment arrives. They are not ideal for recurring cash needs, since you pay interest on the full principal from day one regardless of how much you've drawn.

Learn more about short-term loans for cash flow gaps.

Credit Line

A business credit line gives you a pre-approved credit limit you can draw from, repay, and draw from again — similar to a credit card, but built specifically for business needs. By borrowing against your pre-approved limit whenever a cash flow gap appears, you avoid the hassle and friction of applying for a new term loan several times throughout the year.

A credit line is the most flexible and practical standing solution for SME with recurring, seasonal, or unpredictable cash needs throughout the year — and it's where our flagship financing product, First Circle's Business Credit Line, fits in. It offers a credit limit of up to ₱20 million* with no collateral fees and other setup fees required. Monthly interest starts as low as 0.99%, and you can apply online and draw funds in as fast as 1–2 business days. Same-day withdrawals are available as soon as your credit line is active, and you only pay interest on what you use, and you can reschedule payments if needed.

*Credit approval, limits, and rates granted may vary upon assessment based on existing First Circle policies.

Invoice Financing

Invoice financing allows businesses to advance cash against their outstanding invoices. The lender typically releases a large portion of the invoice value upfront — some of them up to 90% — directly to your business. When your client pays the invoice in full, the lender collects that payment, deducts their fee, and releases the remaining balance to you.

Invoice financing is best suited for B2B businesses that issue invoices with payment terms of 30, 60, or 90 days. The key advantage of this kind of financing is that you are accelerating your own receivables rather than taking on new debt, so it does not significantly impair your future borrowing capacity.

First Circle's Business Credit Line works just as well in financing your invoices. You can draw funds against your outstanding receivables and repay once your client settles, with no restrictions on how you use the credit as long as it's for a business need.

Purchase Order (PO) Financing

PO financing is designed for businesses that have confirmed purchase orders from clients, but don't have enough cash on hand to fulfill them. Here's how it typically works: you submit your purchase order to the lender, who advances the funds to cover your production or procurement costs. You fulfill the order, deliver to your client, and repay the lender comes once your client pays.

It's particularly useful for manufacturers, distributors, and traders whose growth is limited by working capital rather than demand. Ever feel like your business can accept more orders if only you had cash for inventory or raw materials? PO financing may be for you.

First Circle's Business Credit Line also works in PO scenarios because you can draw exactly what you need to fulfill a specific order, repay once your client settles, and draw again for the next order. Just let us know how much you need for a project, and we'll help you get your funds in as fast as 1-2 business days.

Equipment Loans

Equipment financing is a variant of term loan that covers the purchase of physical business assets — machinery, vehicles, technology, or property. Unlike working capital loans which fund operations, equipment loans fund the asset itself, with repayment spread over a longer term.

The defining feature of equipment financing is that the asset being purchased typically serves as collateral. This makes it easier to qualify for larger loan amounts compared to unsecured working capital loans, since the lender has something tangible to recover if repayments fall through.

That said, equipment loans come with some important limitations:

- The asset depreciates over time, so if you default, the collateral value may not fully cover your outstanding loan balance.

- Approval and disbursement can take longer than working capital loans, since the lender needs to assess the asset's value.

If you're looking to finance new equipment or property, our Business Credit Plus is worth considering as an alternative to a traditional equipment loan. It's a fixed-term non-collateral loan of up to ₱20 million with no collateral required, designed specifically for major growth moves like purchasing equipment and assets. You receive the full amount upfront, repay in up to 24 months, and get approved in as fast as 3–5 business days with same-day disbursement — without tying the loan to the asset itself as collateral.

Other Working Capital Instruments

- Post-Dated Check (PDC) Discounting. Businesses can use post-dated checks from customers as the basis for immediate financing — useful when clients pay by check rather than invoice.

- Export Finance. Designed for exporters, this covers pre- and post-shipment financing: either funding the cost to manufacture export goods, or bridging the gap while awaiting collection of export receipts. A Purchase Order or Letter of Credit from your buyer is required.

Learn all about the different types of business financing available to Philippine SMEs.

How Do You Choose the Right Working Capital Loan?

See the working capital loan type that matches your specific need:

Beyond the loan type, evaluate the total cost (interest + fees), repayment term, eligibility requirements, and how quickly you can access funds. For most Philippine SMEs where speed and flexibility matter, an online lender is usually the better fit — unlike traditional institutions, many online lenders don't require collateral, have faster approval timelines, and are built for businesses that can't afford to wait weeks for a decision. Just make sure you're dealing with a legitimate, SEC-regulated lender and transacting only through their official channels.

Need business financing today? Apply for one with First Circle by clicking here.

Frequently Asked Questions

How do I calculate how much working capital I need to borrow?

Add up your monthly fixed operating costs — payroll, rent, utilities, minimum supplier payments — to identify how many weeks (or months) of expenses you may need to bridge.

Then, check your receivables pipeline — if clients are due to pay within the next two to four weeks, that incoming cash can reduce how much you actually need to borrow. In this case, you may borrow the shortfall, not the full computed cost of expenses you need to bridge. Overborrowing increases your interest and monthly repayments without adding any business value.

What's the fastest working capital loan available to SMEs in the Philippines?

First Circle's Business Credit Line can be approved in just 1-2 business days after you submit complete documents. Once your credit line is active, you can draw funds from it in just 24 hours. It requires no collateral and no setup fees — truly designed for short-term bridge financing when you need to plug a cash flow gap quickly.

Should I get a collateral or non-collateral working capital loan?

It depends on what you qualify for and how quickly you need the funds. Collateral-backed loans from traditional lenders typically come with lower interest rates, but the approval process is longer and requires you to put up an asset for security. Non-collateral loans from online lenders like First Circle are faster to access and don't put your assets at risk, making them a better fit for most SMEs that need working capital on short notice. The trade-off is that interest rates for non-collateral loans are often higher. If speed and flexibility matter more than getting the absolute lowest rate, a non-collateral credit line is your best option.

Where should I apply for a working capital loan in the Philippines?

You can apply through any traditional bank or SEC-regulated online lenders. Banks offer lower rates but usually require collateral, take a week or more to process, and are harder to qualify for if your business doesn't have an existing relationship or long credit history. Online lenders like First Circle require no collateral, approve faster, and are built specifically for SMEs and microbusinesses. Whichever route you choose, make sure the lender is SEC-registered and transact only through their official website or app — not through third-party agents or social media.

First Circle Growth Finance Corp. is a financing company with SEC Registration No. CS201605477 and CA No. 1108. It is regulated by the Securities and Exchange Commission with the email flcd_queries@sec.gov.ph. For any questions, you may reach out to support@firstcircle.com.

Jess Jacutan

Open an account today

No paperwork

Online application form in 5 minutes with 3-7 documents required.

No branch visits

Open your account from the comfort of your own office or home.

Same or next-day account opening

We’re supported by a strong ecosystem

We create symbiotic relationships with fellow advocates of SME growth

OUR INVESTORS

OUR PARTNERS

of the Philippines

Commerce of the Philippines

Commerce and Industry

Commerce and Industry

Commerce and Industry

First Circle is trusted by the Department of Trade and Industry (DTI). View certificate

First Circle is regulated by the Securities and Exchange Commission (SEC). For concerns, you may contact SEC at (+632) 8818-5554 or crmd_publicassistance@sec.gov.ph.