The Philippines boasts of the longest Christmas season in the world. Albeit the growing enthusiasm for celebrating Halloween on October 31 — September continues to mark the start of the BER months, which means preparations, sales for presents, and Christmas songs and decorations inside malls’ PA systems are a go.

What that means for businesses, especially suppliers, is that operations will be a lot busier than normal during the BER months. For business veterans, you may have already worked up a plan that fits into your financial structure and operations schedule perfectly well. For startups and new businesses, you may or may not have a plan that covers working capital and other tasks during seasonal spikes such as the BER months and other big Philippine holidays like Chinese New Year, but the usual barrier to meeting your financial strategies is the lack of cash buffers and collateral to use when demand is at its peak and you simply have to turn down a few projects. Nonetheless, even with the financing plans in place or not, both long-running and new businesses will always need to have alternative plans lined up because each year and each season is different. Somehow one reason or another catches business owners by surprise that causes them to scramble for last-minute financing.

Without going into full discussion on the COVID-19 pandemic that struck the global economy early this year, all businesses have been assured of the fact that many business disruptions are still unforeseen. In fact, it could be that your business wasn’t quite sure you would meet your sales projections pre-COVID a month to two months ago but may orders may just be picking up now.

Of course, one of the biggest reasons why Filipinos celebrate the BER months in extended periods is due to money wired in by their OFW relatives who send in their bonuses during this time. Even though the Bangko Sentral ng Pilipinas (BSP) has declared that year to date, OFW remittances contracted by 2.6 percent this year (as of October 2020), this is much better than previous projections that it would contract by as much as 20 percent. It means, economies are slowly bouncing back across the globe. Locally, even if public Christmas celebrations are suspended in Metro Manila, retail shopping is carrying on online and companies will still celebrate with their employees in one way or another.

Despite all the business disruptions that the year 2020 has brought to the Philippine business community (from a pandemic to super typhoons and flooding catastrophes), some jobs to be done remain the same for Small to Medium Enterprises (SMEs), which trigger them to look for last minute financing during the BER months, or at least have ready contingency plans for taking out loans and these are:

· 13th month pay and other bonuses – As mandated by the Philippine government, employers must release the 13th month pay of their employees. Despite the COVID-19 pandemic, the Department of Labor and Employment issued a statement that there will be no exemptions for employers with regard to giving out their employees’ 13th month pay. In fact, they must do so before December 24, 2020. For companies who give beyond the minimum 13th month, bridging this working capital gap may even be more problematic without ready buffers or financing.

· Additional orders – you might be expecting less orders with the announcement of Christmas party restrictions in Metro Manila as well as the general status of our economy, but business is picking up for many and retail has been bouncing back strong, even if most efforts are through online means.

· Hire more staff – to meet the growing demands of your business

· Invest in expansion – expand to more municipalities in the country and export outside the country.

· Pay your suppliers on time – so you can complete your orders on time and take on more after.

· Buy new equipment – to help increase your operational capacity and speed up orders. This will also help boost the quality of your products.

For those of you bootstrapping to keep up with the high demand and take advantage of the growth opportunities BER months provide SMEs, the first tip will come in handy for you.

Tip #1: Always have a separate bank account for business vs. personal accounts

When business owners start their own business, all business expenses are funded by their personal savings. This is usually why sole proprietors tend to mix their personal finances with business finances in one bank account. For one reason or another, opening a separate bank account is seen as an added task that most sole proprietors don’t want to deal with until they reach a certain milestone or when they really have to for tax purposes.

Corporations are mandated to have a separate bank account for their business. Nonetheless, it’s always important to organize all matters related to accounting so you can easily track all business transactions and perform necessary audits with ease, manage your cash grow accurately, facilitate your tax returns filing procedures, establish credibility and professionalism for your business and create a credit score for your business.

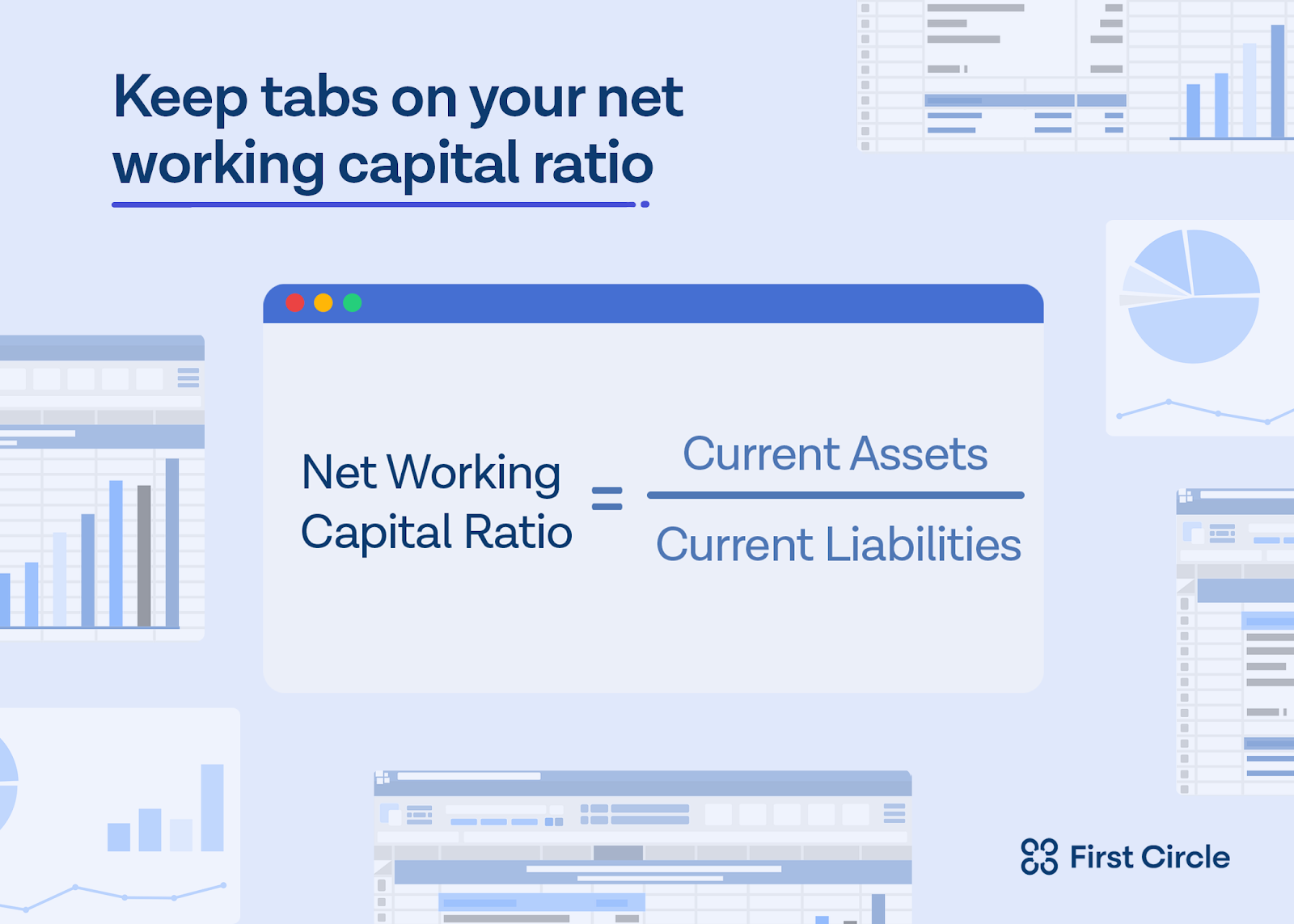

Tip #2: Keep tabs on your net working capital ratio

First off, what is working capital? This is the amount of money a business has to pay off its short-term obligations like rent, wages, raw supplies, gas, etc. Small businesses are no strangers to having unhealthy working capital, which means they find themselves at a point where they don’t have funds to pay for any of the expenses mentioned earlier.

To help minimise these instances from coming, business owners should be keeping tabs on net working capital ratio, with a goal of scoring a 1.0 or less. The ideal score basically says a lot about how you manage your working capital or that you have enough funds to keep your business running despite possible backlogs in receivables. You can learn more about the formula and other ways to keep a healthy working capital here.

Tip #3: Come up with ways to get paid on time or even earlier

It’s best to be proactive when ensuring your payments come on time. Sometimes, setting dates isn’t enough. You have to communicate reminders through thoughtful and well-crafted communications via email or personal call, depending on the nature of your business and relationships with customers. Additionally, make paying a smooth and easy process for them. One way is through make sure your invoices are clear and complete, with no missing information that might cause your client's accounting department to kick it out of the system for further review.

Being proactive doesn’t necessarily mean imposing penalties for late fees. Instead, why not incentivise early payments. This doesn’t just ensure your functional need for good cash flow management, but create rapport with your customers.

An additional tip is to have an organised sheet that monitors your clients’ payments. If you have an online vendor software where all payment transactions are processed, there might already be a tool that allows you to export client reports. This way, you’ll know who always pays late and you’ll be able to focus on reaching out to them or set-up next steps that will improve their repayment behaviour or eventually help you decide on continuing your business relationship with them.

Tip #4: Get online business financing

If you find yourself in a rush, there are always online business loans from online private lending firms like First Circle. At a time when several unlicensed and illegitimate lending firms have sprung up, you can trust that First Circle complies with the Securities and Exchange Commission and the BSP as regards to industry regulations. Last week, the lending firm also renewed its partnership with the Department of Trade and Tourism.

Amortizing Loan

The Amortizing Loans or ALP product is the newest First Circle product. It gives businesses the best value yet. Depending on the nature of your business and the types of orders or the specific need for financing, and payment terms you have, First Circle will assess if you would qualify for an ALP.

This is by far the most custom-fit product that we can offer that gives borrowers control over their installment payment schedule. You can pay weekly or monthly, which benefits the health of your cash flow in the long run as you get to repay early, even securing an interest rebate should you do. So if you need help specifically with the following, the ALP may just be right for your business:

Unlike banks and other business financing providers, you only pay for the funds you use, new and repeat partners can access funds as fast as 1 to 3 business days, with flexible repayment date setting, clear pricing and no hidden fees. It’s also good to note that our ALP product is also the only solution in the market that allows for free repayment rescheduling - there is no charge for moving the payment date later, other than the incurred interest charge.

Invoice Financing

Qualifying for our Invoice Financing product would have less requirements. If you’re a Business-to-Business (B2B) company that has current outstanding receivable, click here to get the summary of our Invoice Financing product and link to how to apply.

The maximum amount you can qualify for depends on the total amount and available credit limit.

Purchase Order Financing

These are usually for B2B businesses that need to buy supplies to fill a customer order but are running short on cash at the time of need. The submission of your purchase order and other requirements can help this vital need.

To learn more about Purchase Order Financing click here.